Founders and funders: what entrepreneurs need to understand about the world of venture capital

Launched in 2012, YourStory's Book Review section features over 250 titles on creativity, innovation, entrepreneurship, and digital transformation. See also our related columns The Turning Point, Techie Tuesdays, and Storybites.

Aspiring entrepreneurs and students wanting to learn about the funding aspects of starting up can find a useful overview in the compact book, Venture Capital Investments, by Raj Kumar and Manu Sharma.

The eight chapters, spread across 165 pages, provide a starting point to the world of venture dynamics. Raj Kumar is Vice-Chancellor of Panjab University, Chandigarh. Manu Sharma is Assistant Professor at the University Institute of Applied Management Sciences, Panjab University.

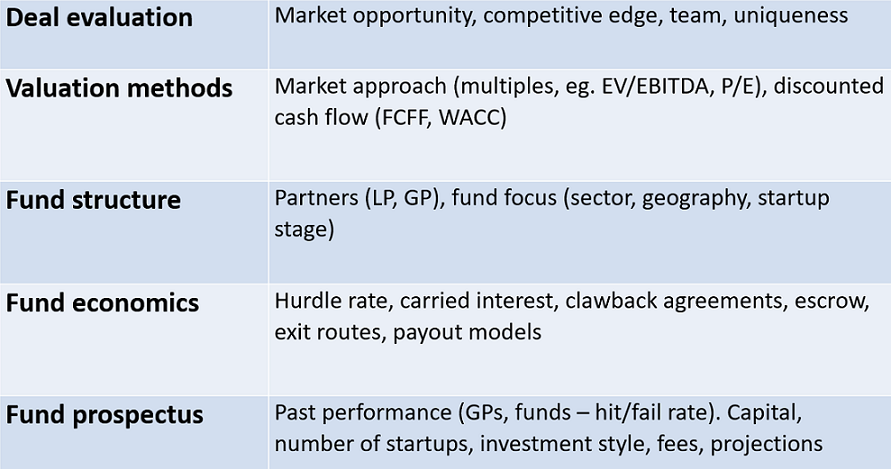

Here are my takeaways from the book, summarised as well in Table 1. See also my reviews of the related books Angel Investing, The Manual for Indian Startups, Straight Talk for Startups, and Startup Boards.

The World of Venture Capital (Table 1 image courtesy YourStory)

Foundations

Venture capital is based on the model of high-risk high-return of investments, the authors begin. VCs bring in not just finance but also management expertise, industry connections, and mentorship support.

This is important in cases where the business idea is new and risky, or the founding team is not experienced or balanced. Early-stage VCs target startups are regarded as too small or risky by traditional financers; as the startup matures, risk decreases but return factors on new investments decrease.

Founders can raise funds through debt (highly leveraged; stakeholder value maximisation) or equity (less leveraged). The choice depends on factors like market conditions and type of industry and company.

Factors like liquidity, information asymmetry, and cyclicality define VC engagement, which can last for around 7-10 years in a startup’s lifecycle. “Venture capitalists follow the Pareto principle – 80 percent of the wins come from 20 percent of the deals,” the authors explain.

Deal structures vary in formative, mid-life, and expansion stages of the startup. “VC firms get rewarded for making accurate predictions and identifying a pattern before it becomes a trend,” the authors observe.

ALSO READ

These 4 homegrown VC firms have helped shape the Indian startup ecosystem into the powerhouse of today

Market growth

Two chapters trace the rise of the VC industry in the US and India, and map portfolios of VCs in India. The IT industry in the 1970s marked the growth of VC as an asset class in the US. In India, early venture financing was done by the government before formal recognition to private investors was given in the 1980s, the authors explain.

Tech and business clusters in China and India grew as investment destinations for many Internet-sector investors from the 1990s onwards. VC-funded startups have helped increase the “absorptive capacity” of business for new innovations.

The authors track some of the deals of VCs in India, such as Inventus Capital Partners (PolicyBazaar), Accel Partners (Flipkart), Nexus Venture Partners (Snapdeal), IDG Ventures (Yatra), and Sequoia Capital India (JustDial).

The journey is not always smooth, particularly when multiple investors are involved in a startup’s evolution. For example, discussions in 2016-2017 for a proposed merger of Snapdeal and Flipkart failed to get an approval of all investors.

Deal evaluation

VCs tend to look for industries where lower investments can lead to large exponential returns with enormous margins, the authors explain. They examine the size of the overall market, and what percentage can be dominated by the invested startup. VCs avoid saturated markets with large competitors (e.g. Coca-Cola, Pepsi for carbonated drinks).

The startup should have a balanced team capable of creating uniquely differentiated offerings, pick profitable price points, develop deep customer relationships, and create entry barriers to future competitors.

In the long run, brand equity and external advisors or partners help in growing the market as well. Other factors in keeping with the times are environmental sustainability and eco-friendliness, the authors add.

Based on these factors, agreements specify the amount and purpose of funds, working and runway capital, burn rate, and monthly cash flow.

ALSO READ

[YS Learn] 5 must-read books before you raise funding

Valuation methodologies

One chapter packed with equations and tables shows valuation techniques in action. The market-based approach is based on multiples and ratios of enterprise value, earnings, revenue, price, earnings, tax, depreciation, and amortisation.

Based on this, VCs calculate required rates of return, fund performance, and shareholding patterns. This applies to pre-money and post-money stages in multiple rounds.

Discounted cash flow-based valuation determines the present value of free cash flows to the firm (FCFF), the authors explain. Factors like the nature (equity/debt) and the amount of capital raised come into play here.

Common equity and preferred equity have different implications for voting rights and dividends of shareholders. VC portfolio parameters include amount invested, amount returned, exit status, and exit multiples. Based on the performance, success can be “normal, grand or super”, the authors describe (in addition to failure, of course).

ALSO READ

Stubborn founders won't go far, the ones with conviction will: Rutvik Doshi of Inventus Capital

Fund structure and economics

Two chapters describe VC fund structure and economics. Limited partners (LPs) are usually institutional investors such as endowments, insurance companies, pension funds, foundations, family-owned offices, or investors with very high net worth.

LPs do not make decisions on how exactly VC firms manage the funds raised for startups. General partners (GPs) raise and manage the VC’s funds, and extend services for startups. Portfolios are business strategies to attract investors, the authors explain.

The authors describe investment steps like business plan submission, meetings, due diligence, and term sheets. Some founder tips on negotiation and dispute resolution would have been a welcome addition to these chapters. An actual or hypothetical case study of fundraising activities of a startup through its journey would have also helped.

Exit routes of an investment are usually an IPO, acquisition, management buyout, or sale of shares to another investor. The authors show illustrative tables of payout models for multiple LPs and GPs, along with an analysis of management fees.

The last chapter of the book describes how a VC raises funds via a prospectus presented to LPs. The prospectus describes the track record of the GPs, performances of its earlier funds, fee percentages, number of startups targeted, and anticipated returns.

Overall returns and riskiness of past performance are assessed by LPs. For example, there may have been too much dependence on the success of only one startup instead of a few startups.

The book ends abruptly with this chapter. It would have been great to end with some suggestions or advice for founders and aspiring investors, or with some analysis on emerging trends and developments.

Edited by Saheli Sen Gupta

Want to make your startup journey smooth? YS Education brings a comprehensive Funding Course, where you also get a chance to pitch your business plan to top investors. Click here to know more.

Original Source: yourstory.com

Visited 599 Times, 1 Visit today